US National Banks App Performance - 2022 A Year in Review

Executive Summary

Citibank takes out the Number One Spot in the US Nationals market segment for 2022 in the Touchpoint group Engaged Customer Score (ECS) Rankings with an average ECS of 4.6 out of a possible 5.0.

This top performer also has been in the top two apps in the entire US market all year in 2022 - A very close second to US Bank.

Citibank and Bank of America both get an award for consistency as their rankings and Engaged Customer Scores have stayed incredibly consistent over the year and have not been hit by the fluctuations of others.

Looking at Citibank, it is easy to assume that everything is as good as it gets. However, we can see in the verbatim customer feedback that there is room to do even better, as the customers are great at picking up glitches that affect their journeys.

Wells Fargo, for example, dropped from 3.9 to as low as 2.5 out of 5 in Feb after a major UI release. The good news for Wells Fargo is that they have gradually clawed their scores back up to an average of 3.9 again and finished the year strongly in 8th place overall. We have seen dramatic score drops in other regions as well when major UI changes are implemented, so the Wells Fargo situation is not uncommon. Learnings we have found from these situations is that far more time, effort and frequency of communication needs to go into preparing customers for the changes and guiding them through as the overwhelming majority of negative feedback comes from users unhappy with navigation, useability, and unable to find or do things they could in previous versions.

We expect to see big things in 2023 when it comes to investing in “In-App Experience” as most institutions are becoming hyper-aware, in the current economic climate, of cost control and mitigating churn risk. The better banks understand customers in app experiences and feedback, the easier they can mitigate churn and reduce demand on call center operators.

We estimate for the US banks, an effective program being implemented to monitor and learn from customer feedback can have up to a 2% reduction in churn and a 1-2% reduction in call center costs (which can add up to the hundreds of millions of dollars saved or retained each year).

Touchpoint Group is a customer intelligence company utilizing advanced AI and natural language understanding in its proprietary analytics platform to analyze over a million banking app reviews each year in its global ECS index.

Touchpoint Group processes customer feedback data captured using internal customer experience platforms and sources. Data is updated daily, with insights available to identify issues for Operational teams, monthly reporting for Leadership teams, and a Mobile Customer Experience Analytics (MCXA) report published quarterly for Executive leaders to benchmark performance by category and against the best in banking app performance.

Video Transcript

-Welcome back to another Touchpoint Group Insight Session. We're looking at the U.S National Banks and while we're already into 2023 but we're going to look back at 2022, a year in review and look at the top stories, the top banks and the things that really stood out for us over that period. Tony Patrick, really looking forward to the insights on this because it was a massive year in the U.S.

-It was, Glenn. Thanks very much. So yeah, today we're looking at the U.S Nationals. Citibank, Bank of America, Wells Fargo and Chase. Now, and this time around we actually will do a comparison across North America in this review as well just to see where they sit.

Let's see what's happened. Let's kick off with our normal approach which is just looking at how these trends have gone across the whole year. One of the things we can see here is there's two sitting at the top here which is Citibank and Wells Fargo sitting there at the top at around -above 4 at 4.2 and about 4.6. So, doing very well and very consistent.

The other one is looking at Wells Fargo about their app change about February-March last year and how that sort of improved across time up until December where it's now, it's matching what it was about this time last year. It's taken a while to get up but they have actually improved up there as well and we saw last time around the drop which was as we saw for Chase they have picked up to some extent but they are still in some sort of trouble there they need to improve things from there as well.

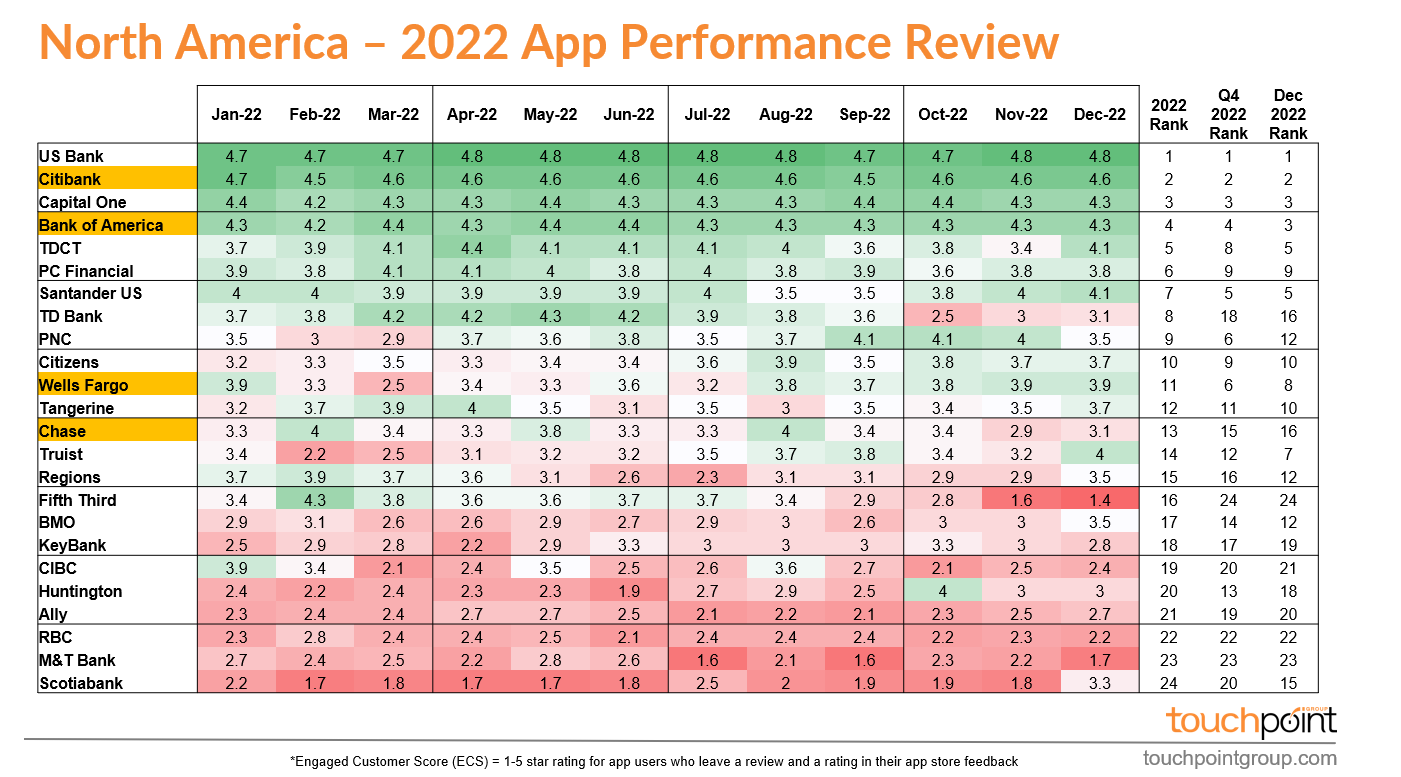

Let's have a look at this for Consistency across the year in the North American Market. So, here's a table... there's a lot just suddenly appeared in front of you, but I suppose one of the things you can have a quick look at is the colour coding there. You can see at the top there, there's five or six which are basically always green, at the bottom there's a similar number which are basically always red and you can see in the middle there's a mix of things going on.

So, if we look at the banks we're covering today in this U.S Nationals, we've got Citibank, Bank of America, they're clearly in the top tier in terms of the U.S, in terms of all North America -we do have some Canadian banks in here as well. Above them, is U.S Bank and that's consistently number one, that's one of the leaders globally, they do very well. I'd like to give an award -a virtual award to Citibank for their scores across time. They've remained very high and done very well and and they haven't been hit by some of the issues that other banks have so well done to them.

Also I'd like to give probably both Citibank and Bank of America Consistency awards because they've remained at that level and they haven't dipped down, they haven't experienced those major issues that others seem to have had across time, they kept things under control to some extent.

The biggest story which I mentioned up front was around I suppose Wells Fargo with their drop away in February and March last year and they have actually increased. It's been a slow sort of gradual increase, but they have now picked up to being there sort of around up towards 4 -they haven't hit 4 yet in the last year so hopefully they can do that in January and February to get things back to a level they're expecting with that new app release.

Right here are the ranking across 2022 for all of North America and also the the Q4 rank, so you can see some things have moved in comparison and also how they did in December in there as well. You can see in general those top three tend to remain in that particular order all the way through as well.

You might recall this is our SURF Analysis, looking at Security and Authentication, Usability, Reliability and Functionality. Now, these numbers here of course, we need to have these as low as possible because these are the pain points, the major pain points customers are having when they're using your app.

One of the things we can see is for Citibank this is why it's doing so well, it has got these numbers down to a controllable level. In particular for both Bank America and Citibank this Authentication piece is down around 2%. It's not very many people have issues with logging in and things like that.

But across the board we can see that the other two there, Wells and Chase, they do have those issues across the board and consistently so but of course Wells has improved in the second half of the year so this number for the second half of the year will be lower for them, but overall there needs to be Improvement across the board in that sort of logging in Reliability when they're using those Journeys as well.

Let's have a brief look at Citibank who's doing reasonably well, or very well globally, we can even jump in and just have a look at some examples. So, they've still got room to grow which is really good because there things you just think they must be perfect -Well not really. They've got people talking about: "The apps keeps crashing... The Sign In doesn't work... Every time you enter ID and password it says... Fix the issue please!" Again, there's still issues but they've been limited which is really really positive for them.

Let's move forward and have a look at one other thing here which is looking at the journeys. Now, looking at these Core Journeys... This is something that customers see as Core Journeys. These are the ones that they talk about with a positively or negatively -they talk about these things as the major things they're trying to achieve with a banking app.

Things like, Depositing Checks, Making P2P Payments Etc. Now, these are the actual average scores when people talk about these particular topics and one other thing -and of course, here the higher is better.

You want to get as high as possible in this case. One of the things I can see here particularly for Citibank, is that they're doing very well on Transferring between Accounts, Paying Bills, Monitoring Account Activity and Checking Account Balance, and we can see that they're above 4 and in some cases 4.5 although they're not doing as well they're not dominating their Cheque Deposits or making P2P Payments. Obviously, some room to improve there for them as well.

What I'd like to do now is have a look at the year in review of U.S Nationals.

Citibank

Across the year I can look at Citibank and see how well they've gone in terms of the conversations going on inside across the year. What's the general conversations going on here? what I can do is have a look at this from this perspective here and have a look at it and see in general we can see it's all positive, so the colouring is very helpful. This is where they dominate: Good service Channel, Good Digital Channel, The App Operates Well, There's Good Features and Functionality and Payment Process. So it's very very positive. You can see the vibe there is essentially very good.

Bank of America

Let's have a look though -let's go down and have a look at the next one here which is obviously Bank of America. So, slightly different. We get a very similar view in terms of things like Good Digital Channel. We even get things like Good App Security, Good Financial Services Provider, but a few things start to pop out in Red so for example which is why they're in second place things like the Account Balance feature is in red there, basic things like checking your account balance is not quite up to par and things like Funds Transfer are slightly lower than average in there as well but again, overall very positive.

Chase

Let's do a similar thing and go down to the next level which is Chase. Obviously, from what we've seen in the earlier data we're going to see a very different story here. Things like Poor Open and Authenticate, Poor Service Channel... Poor Authentication and things like that. You can see clearly here, there's been some issues with Logging in and things like that. Let's have a look at Wells who obviously had sort of two halves to the year and they've done better in the second half.

Wells Fargo

We can see in here, for them it's very different though we've got sort of some Tech Issues so Tech issues are the things that make them Stand Out across the year. Open and Authenticate and Security.There's a few bugs and things so again, we think that they have those more under control this time around in the second half of the year, but they need to continue to improve on these as they move forward.

So there we have it. A summary in review across the year. Thank you, Glenn.

-Yeah absolutely, Tony. And the think 2023 for me looking ahead is actually in and around using the sort of data to create efficiencies and cost savings in the business and reducing that customer churn. If we can look at these things and improve that experience, the volume of call center complaints, the number of call center calls that they're needing to support, as well as that customer churn with people leaving the app and leaving the bank are going to dramatically reduce and 2023 we know out there in this industry that reduction of churn and cost savings is going to be a massive focus for many banks out there. I encourage you all to reach out to us if you wanted to have a chat and if you would like a copy of that ranking chart looking across North America, please send us a message more than happy to send it out to you. Have a great day folks.