UK Legacy Banks Banking App Insight Sessions January 2023 – A Year In Review

Executive Summary (TLDR)

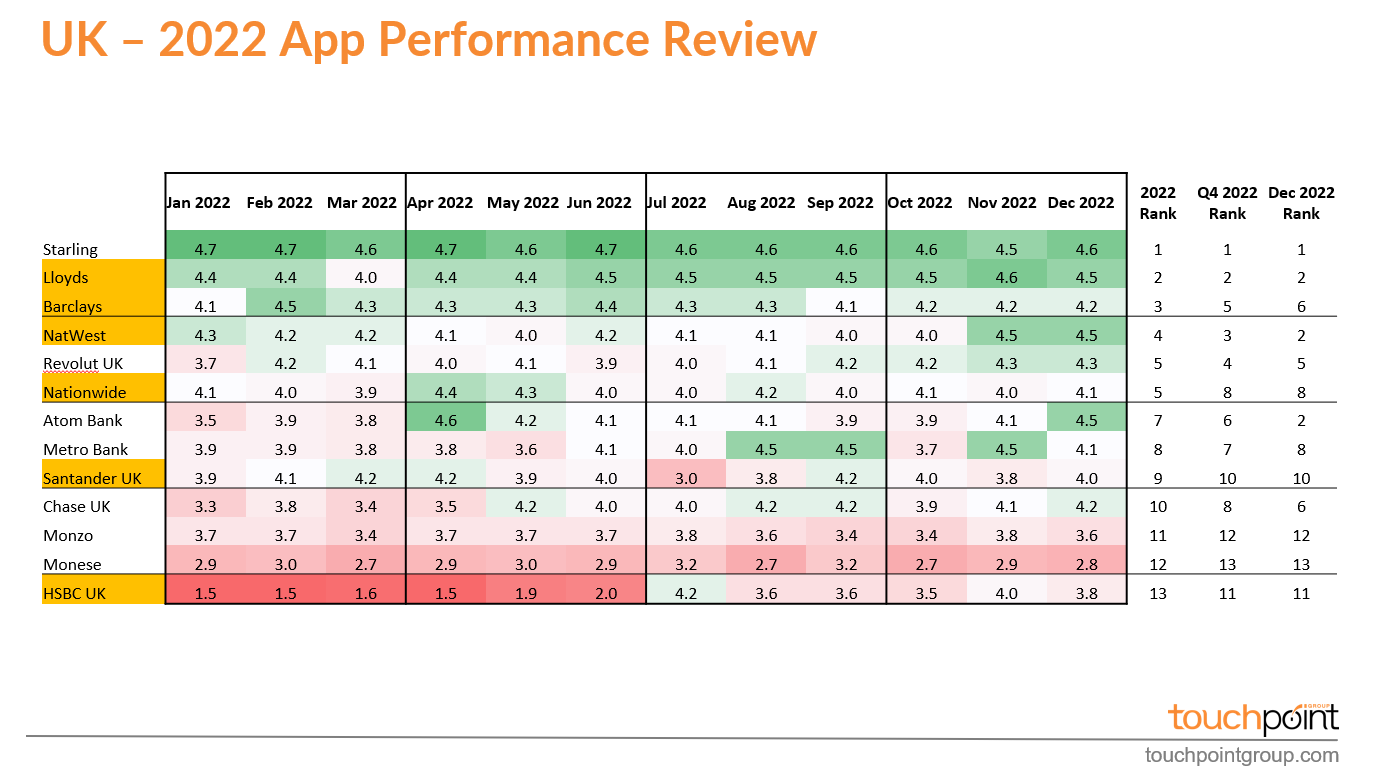

Lloyds Bank take out the Touchpoint Group overall top performin App for Engaged Customer Score (ECS) in 2022 and have been one of the most consistent performers in this market segment.

It is rare to see a dip in ranking or score for the LLoyds Bank app and while they still have a bit to do to catch Starling Bank in the overall UK market, the app is right up there with the Global leaders. The question for 2023 for Lloyds is how are they going to maintain their position with many of the competitors investing heavily in improving their apps.

A classic example of investment leading to impact is HSBC who take out the award for most improved app for 2022. While they are still in the bottom spot, the trajectory the app is on is promising and it will be great to see the impact of continued impact into the app over 2023. With cost control and churn mitigation a big factor this year, app performance and customer feedback will play a big part in helping HSBC achieve their goals.

Barclays has been another consistent performer in 2022 however they have fallen victim to flatline performance. While good and steady, other competitors have invested, developed and out performed Barclays in 2022. Barclays slips from 2nd in national rankings in 2022 to finish the year in 6th place, overtaken by NatWest as well as Atom Bank and Revolut. Two of th primary issues impacting Barclays Engaged Customer score are contactless payments and poor cheque deposits.

Santander UK have been steady performers in the middle of the pack finishing the year in 5th for the Legacy Bank sector, just above HSBC and 10th overall in the entire UK Banking App sector (once we include the Challenger Banks that are investing heavily into in-app experiences). Santander are well placed to invest in this area in 2023 and seriously improve rankings, ratings and most importantly customer experience leading to greater retention and lower cost of service.

We expect to see big things in 2023 when it comes to investing in “In App Experience” as most institutions are becoming hyper aware, in the current economic climate, of cost control and mitigating churn risk. The better banks understand customers in app experiences and feedback the easier they can mitigate churn and reduce demand on call center operators.

We estimate for the UK banks, an effective program being implemented to monitor and learn from customer feedback can have up to a 2% reduction in churn and 2-3% reduction in call centre costs (which can add up into the hundreds of millions of dollars saved or retained each year).

Touchpoint Group is a customer intelligence company utilizing advanced AI and natural language understanding in its proprietary analytics platform to analyze over a million banking app reviews each year in its global ECS index.

Touchpoint Group processes customer feedback data captured using internal customer experience platforms and sources. Data is updated daily, with insights available to identify issues for Operational teams, monthly reporting for Leadership teams, and a Mobile Customer Experience Analytics (MCXA) report published quarterly for Executive leaders to benchmark performance by category and against the best in banking app performance.

Video Transcript

0:01:00 – Glenn Marvin: Thank you, and welcome back to another Touchpoint Group Insight Session and we are looking at the main Banks in the UK and we're going to have a look back at the year 2022 in review. A big year for most and Tony Patrick, let's jump straight into it and really get the dish on what happened in 2022.

0:24:02 – Tony Patrick: Yeah, thanks Glenn. So looking today at the UK major Banks so Lloyds. Barclays NatWest, Nationwide, Santander and HSBC. Let's just jump straight in see what's happened, so who are The Story of the Year?

As you can see there is HSBC well it's a major Improvement from June to July, that's the biggest Improvement we've seen across any of the banks. Although the biggest Improvement means they weren't doing too well in the first place but, again, it's a big Improvement. Let's just change the scale in this and move it to the past six months so we can remove that movement there from HSBC so one of the things that, you know, although HSBC has improved they are still sitting lower than a lot of the others they're compared to or up against in a sense, so they're still sitting around 3.8 compared to others. But, you know, the likes of Lloyds has been so consistent across the year, NatWest has picked up in the past few months really well like just above four to about four and a half so, a very good improvement from them. Let's move ourselves forward though and have a look at how that compares to others.

So just looking at the major UK Banks here. So, Lloyds is doing really well, although there's a few, you know, drops across the year so, an award goes out to Lloyd's from my perspective about their consistency in this particular category across the year for these major Banks. Barclays has also done reasonably well they're sitting just behind Lloyd's and their consistency is pretty good so the major gap between 4.1 and 4.5 but reasonably good consistency across the year. We also see Santander is sitting there. They've sort of remained reasonably flat across the year.

Now- and as I said you can see the sort of clearly the red zone for HSBC at the start of the year to their Improvement at the end of the year. But again, as I said that hasn't changed thinking marks, the rank is 13th overall but only remains 11th in December and in the last quarter so, although it's an improvement, they've improved to be just below the others, they've still got some room to move to get to that next level. Let's have a look though at why, you know, what's going on here.

So, those of you who are sort of regular listeners you can see in here what are the things we look at here is what we call our SURF Analysis, and this is around Security which is about logging in and things like that, Usability which is User Interface and being able to use the app properly, Reliability and Functionality. So, clearly, we can see that HSBC hasn't done that well across the year in those areas. But, we can see though why Lloyds is doing so well, it has actually, for example, Security and Authentication it's down to only 3.1% of people mentioning this is an issue. Again, these are problem areas, so you want these to be reduced as much as possible. So, doing pretty well there and Usability is down, 6.5 which is great they're actually pushing things down to a new level. So Lloyd's is the one to look out for amongst this particular group to improve on.

Let's have a look at the year in a review of Journeys. Now, this is a slightly different perspective in that what we're looking at here is when people mention each of these types of Journeys like Checking Your Account Balance, Monitoring Account Activity, Transferring Between Accounts. What we want here is a higher score so people are happy with that experience. We can see here that HSBC is, you know, when they've got sort of technical issues these obviously flow on to these Journeys as well we can see they're having issues across the board. Whereas, when Lloyd's customers actually are working with these areas or using these Journeys, they're actually having a very positive experience. Particularly things like Making P2P Payments, they definitely stand out compared to others, so others need to pick their act up and look at Lloyds to what they're doing in this particular area. So a very positive move across the board.

Let's have a brief look though at, you know, what's the big stories coming through for each of these Banks. Where do they stand out compared to their competitors? So this view we've got here is actually looking at the big conversations coming through from each of these particular topics. So, this is looking at Lloyds. Very big green coming through is the general experience here: Good Service Channel, Good Mobile App... it's Good, it's Great to Use, it's Easy to Navigate pops out as well. So very positive view coming through. There's a couple of small things: the App Logout Feature in general, that means people being logged out without wanting to and some issues with passwords. But in general, we can see that's very green. Let's move along to one that's sort of similar.

So, Barclays is doing really well. I'll just jump into that one and look at this sort of top level to see how they're going and I'll look at a couple at the bottom to see how they're going there as well. So again, even though Barclays is near the top we can see there's room to improve to go to that next level. So it's Fast, there's Good Service, it's Reliable, it's Efficient... yeah, great, but things like Paying by Cheque is slightly it's below average. Moving money, so Moving Money is a very -it's a broad topic around moving money around the app, there's sort of some issues coming through there and that could come through things like Poor Cheque Deposits and things like that. So again- and even things down here about Contactless Payment Issues coming through as well. Reasonably positive, but still some negative things popping through.

Let's move down to the other end of the scale. Obviously, HSBC we saw across the year. Let's look at them, because we can- it's a nice, you know, clear comparison about what's going on in this world. So again, there's, you know, lack of- there's issues with App Updates, there's App Crashes, there's Technical Issues that was what was happening at the start of the year, so it's a thing they've actually fixed at the second -or to some extent- in the second half of the year but still room to grow for them in this particular area. So, major Technical Issues across the year. And just one more while we're here, is just having a look at the sort of middle of the road here Nationwide yeah they're doing reasonably well, but let's have a look at their score is 4.1 but there's a few things coming through where they can fix things. So things like this, Issues with a Card, Transferring Money and add PE details. So some issues for them to fix up along the way to actually do. So again, there's no big major Technical Issues popping out here for me but it's around just fixing those Journeys to make sure they're functioning well for customers. So, a big year for this group and there's a lot of room for improvement as well. So, thank you, Glenn.

7:10:18 – Glenn: Thanks, Tony. And if anybody wants a copy of that ranking chart where we look at the entire UK market and segment it into how they performed over the year, over the last quarter and in December feel free to sing out and we're looking forward to a 2023 of growth for all.