In this month’s snapshot of UK legacy banks, there is much to learn from both the laggers and the leaders. Join us as we delve into what is taking place across the category.

A lesson in never resting on your laurels until you know the full picture

HSBC’s dramatic upswing earlier in the year aside, the banks within the UK legacy category have, for the most part, maintained consistent Engaged Customer ScoreTM (ECS) rankings for some time. Santander on the other hand, has experienced a series of fluctuations followed by a big drop down in July. We begin the October snapshot with a look into what has been the cause of these fluctuations for Santander.

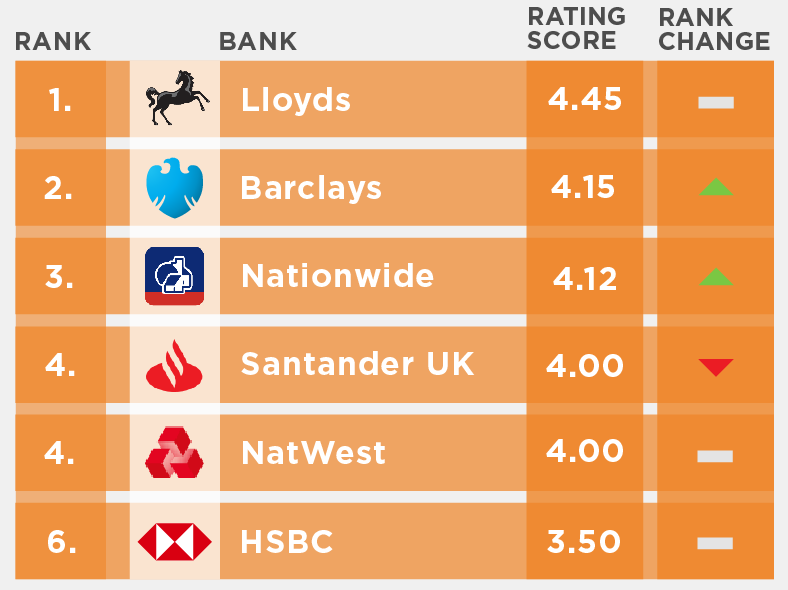

UK Legacy banks Engaged Customer Score performance rankings for October 2022

To provide context to the situation, we take a brief look at the global rankings for Quarter 3 (July-September). This provides a view of how well the UK and US banks are performing against each other. The highest-ranking from the UK legacy category is Lloyds in 4th place. Santander UK’s ECS of 3.5 puts them in 29th place, which is the lowest position for the UK legacy banks in the global rankings.

Looking specifically at what has been going on for Santander from a launch perspective, we can see they have some fluctuations around releases, indicating that a more frequent release schedule could help them get on top of issues that may be affecting their ratings in a timelier manner. This approach would be in keeping with others within the category, as demonstrated by the example of Lloyds who have a consistent monthly release schedule.

Tony isolates the ECS to October 2022 to look at what differentiates the banks within the UK legacy category and provides further detail into the impacts of the various themes unique to each bank.

HSBC customers are talking about log out issues with a previous app version. The issue may appear to be a small thing; however as displayed in the Review Rating Analysis tool this is over indexing for HSBC indicating it is affecting their scores in a bad way.

Barclays appears to be sitting comfortably with an ECS of 4, however all is not what it seems as Tony reveals that they're having some issues with app updates, bugs and the app payment features are a problem for people.

By contrast, Lloyds has a very good ECS of 4.5 and as demonstrated in the Q3 global ECS rankings, they are one of the top performers by global standards. With good app usability and performance shining through the comments, Lloyds provides a fine example of what best practice looks like and where the others in this category need to aim for.

How well does your bank perform and how well do you really know the full story? Reach out to the team at Touchpoint Group for a customised review that will give you the intel.

Full Transcript

00:00:02 – Glenn: Hello, everybody, and welcome back to another Touchpoint Group Banking App Insights Session, and we're moving across the pond, as they say, looking at the UK Banks, and this very traditional segment has... -while there have been fluctuations in the actual ranking scores for each of the individual banks, there's been consistency in the actual ranking positions for quite some time. So, let's look at customer sentiment and the things coming through showing why they're ranking where they are—Tony Patrick, over to you.

00:00:48 – Tony: Great. Thank you, Glenn. So, today we're looking at UK Banks so, Lloyds, Barclays, NatWest, Nationwide, Santander UK and HSBC UK. So, let's just jump in and look at our normal perspective on how these scores are going, and what's going on.

Yeah, one of the things we've seen previously now, I'll -is the HSBC jump in July -a massive jump in July, but that has gone down a bit and softened, and they're sitting at around 3.5 month on month. So, in essence, apart from that jump up, they've retained their position as in place in this particular data set here, so what we're looking at here is also there's one of these banks here, like Santander, does have a bit of fluctuation going on they did jump down in July. But you can see elsewhere they're moving down as they dropped in May; they've jumped back up twice from August to September and down slightly in October. You know, again, there are some variations coming through there now as compared to others we're seeing and also compared to what we can see up here with Lloyds since, you know, one dip in March but pretty much it's fairly flat across time. So, doing very well in what they're achieving in terms of that -I'll just remove HSBC so we can get a bit of a feel because that ruins the scale to some extent.

But we can see here that sort of movement is it extenuates the movement when I change the scale but again, Lloyds has pretty much remained fairly flat at about 4.4 to 4.5 across time. But, what I might do is there's interesting one of the things we can see the fluctuations happening for Santander. Let's have a quick look at their Release Schedule. So, let's have a look at what they're up to. Before I do that -actually, this is interesting, so before we even step into that, just some context globally or this is just a 'UK/US-Centric' view but, just having a look at where the UK Legacy Banks sit here so looking at Lloyds, which is our first in this particular category at 4th, Barclays 11th, we've got here then Nationwide and that we're sitting there at 4.1 each, HSBC UK at 4 Santander -and this is the -this is Q3, mind you, so this was when Santander had that big drop, so it actually didn't include but, now they've actually picked that back up. So, it gives you a context cell about where they fit and how they scale across from a global perspective.

But, what I want to do, as I mentioned before, is have a look at this from a launch perspective. This is Santander which we see they have some fluctuations but, this launch cycle here, it's not- I wouldn't call- it's not chaotic in any sense, but it does it's infrequent is probably the best way to describe it. So we have a release in February we then have one in potentially April-May this green one here at 4.2 we then have one in June coming through at -this is 4.2. It's an update 4.20.6, And then another one coming through in August 4.21, so it looks like a sort of every two months then Santander will come through and make that change. So, this. Let's compare this, though, to Lloyds in this category, and one of the things you can see here is pretty much consistency. Pretty much every month, you'll see a spike in a version coming through, you know, 8 you know, 85, 88 is a sort of an 80-86 in between. Every month there's sort of a launch coming through of various app versions. Now, for both of them it's pretty good because some others we see we see sub versions popping through as well as they try to fix various things coming through for both of these that doesn't tend to happen we tend to so, if someone uses this version it sort of drops away, and then they upgrade. So it's a -really, it's a positive thing.

Potentially for Santander that release cycle could be opted frequency just to make sure they're on top of things as they move forward. What I'd like to look at though, is what makes these Brands different. This is looking just October. What are their scores. So, looking at -we saw these upfront anyway but, HSBC sitting at 3.5 Lloyds sitting at 4.5 up there as well. So let's have a quick look through from a higher level perspective what's actually going on with HSBC.

One of the things we can see is that customers are talking about a previous app version. They're talking about things like a date of birth, bad logout of the app, for example. So we can even dig into these. Now, these are reasonably small because looking at one month and one very specific thing, people are having trouble putting in their date of birth into the app. It sounds like a small thing but, HSBC, they're over-indexing in a bad way on that particular topic. What we can also see if I go back to my area across here, is we can also see something in here about block bad log out of the app. So if I select that and have a look, I can quickly get a feel of this. So, it logs people out as they're trying to do things. You know, not a very interesting thing for the customers: in the middle of something and they're trying to log them out straight away. So again, there are some areas to improve for HSBC, and potentially, they can sort of understand this a bit more detailed to fix these things as they are consistently below the others.

Let's jump forward again into another one which is Barclays. So again, their score is a lot higher sitting above 4 but, that doesn't mean they don't have any issues there are still things going on in here compared to others where they do over-index. They're also having some issues with app updates they have issues with making payments, etc, and also some with app bugs. Interestingly, what we see with the likes of- when Banks get above a certain level, potentially even 4 and above and they have things like their bugs and Security in order and login issues in order to some extent then, their actual Journeys can shine. In this case, though, we're not seeing that. They have -they still have some bugs but, we suddenly are seeing making a payment by the app is still a problem and then, yeah generally the app payment features a problem for people, so they still need to pick up on these things that need to improve on. These should have started to shine, but in fact, they haven't. So that shows us these are a problem even though customers can get to them, they're causing an issue for customers.

Let's actually move forward, though and have a look at Lloyds. So Lloyds is up there in terms of one of the global better players, and here you can suddenly see in this case here they do have their login and their bugs under control; then suddenly you see things like good app usability, good app performance, and all these things coming through like the basics of "I can now try a good transfer between accounts", "a good account to account transfer" so this is the type of thing Barclays could actually get to if they understood their Journeys in a bit more detail that can actually push that to the next level. So again, this is a sort of thing where others can learn about, you know, what best practice looks like and where you need to focus, so getting the foundations right is one thing, but if your Journeys aren't performing, you're going to hit another barrier for customers as they go through that process. So, lots to learn in here and particularly from Lloyds but HSBC are probably the sitting behind, and they've got a lot to catch up on in this category.

00:08:19 – Glenn: Yeah. Thanks very much, Tony. You can learn just as much from the laggers as you can from the leaders. So great insights there, and if you want to have a chat to us about your banking app, feel free to reach out to Tony or I.