Exec Summary

The recovery of the Wells Fargo App since the UI update in Feb seems to have stalled. Some good signs of recovery in April, but customer sentiment has completely flattened off since and the app is still sitting on 3.3, well below the average scores above 4.0 the app has traditionally sat at prior to the update.

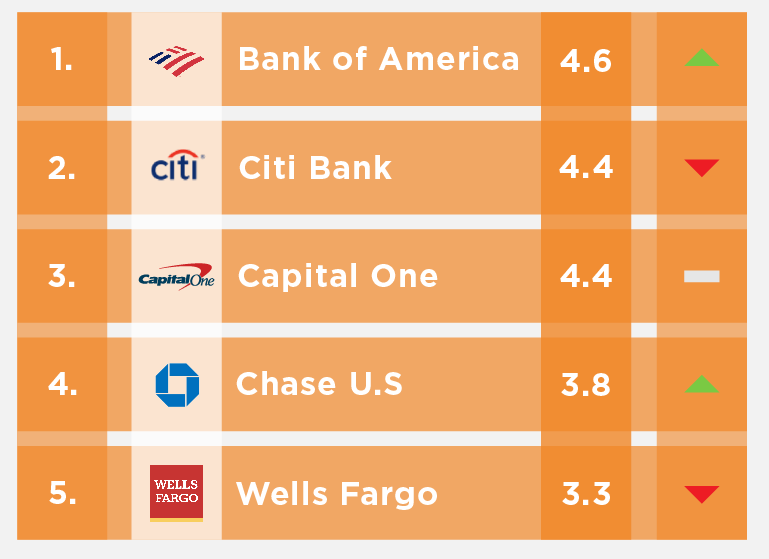

U.S. Bank and CitiBank continue to lead the pack, and where they have traditionally tracked very close to each other in performance, U.S. Bank is beginning to open a performance gap on CitiBank at the top of the table.

Deeper Dive into Chase US

Historically the Chase App Engaged Customer Score has averaged around 3. There have been performance spikes with the ECS in Oct 2021 and Feb 2022 up to 4, and May performance indicates another lift in Engaged Customer Score. The lumpy ECS rankings also indicate a reactive approach to issue resolution that could be improved with a data-driven approach, prioritizing proactive work to keep performance and customer sentiment consistent and improving.

In May there has been a significant improvement in customer sentiment on reliability issues with negative sentiment dropping from 16% of all engaged customer ratings dcown to 10%.

Good gains have been made in the area of Cheque Deposits and App Payment features in May and there are still opportunities to close the gap on market leader U.S. Bank in Cheque Deposit (gap of 1.3 rating points), App Payments (gap of 0.8 ratings points), and the View Transactions feature (gap of 1.6 ratings points).

May 2022 Engaged Customer Score Rankings

Note: A deeper dive is also possible on all these features to identify exactly what actions could be taken to make improvements and close the gap.

If you would like a free personal deep dive insights session on your banking app performance feel free to book a discovery call

Full Video Transcript

00:00 Glenn: Hello everybody and welcome back to yet another Touchpoint insights session, where we're looking at the US Nationals market in regards to their banking apps, and really the theme for May is, the chase is on. In both the UK market and in the US Market Chase have been doing some pretty interesting things that have led to some quite significant improvements in their Engaged Customer scores and Tony Patrick is going to do a little bit of drilling down and having a look at what they've been doing and where they could be going. I'm not going to muck around Tony. I'm going to hand it straight over to you and we can rip into it.

00:43 Tony: Brilliant. Thanks, Glenn. I'll just jump in and share my screen. So I'll share this window here and we can jump straight in, so that should pop up any second. So, what we're looking at here is just the, what we're covering today as the US National banks. So, Wells Fargo, Citibank, Bank of America, Chase, and Capital One, and obviously there's some others in the series - US Tier One banks and US Regional banks, let's focus today on US National banks. So, our normal view we have with this is having a look at what the trends have been. Now, just a reminder for those who may have seen this for the first time we use what's called an Engaged Customer Score. So that's those customers giving a score and a comment. That allows us to have a really sharp view of this data, any changes that are happening are real. We aren't getting lost across time with sort of a bulk of this information that's not useful to us.

We focus on those customers who are telling us the things about the app, and that allows us to see these changes. Like we can see here Wells Fargo had that dip happen, and we saw that very early on it sort of dipped early on and went down. Now, one of the things with Wells Fargo is we've seen that it actually dropped significantly into March, but they did some work. We talked about this last month. They did some work to pick up in April and obviously they were getting above 4 for most of this year until that drop happened. We expected them to bring that up reasonably fast. You can do that in one or two months in general to turn that around, but they've, they seem to have flattened out here in May. We can see that they haven't continued that rise. They’ve still got some similar issues they've had in the previous months. So some pickup there for them,

02:29 Glenn: Quite a significant gap from the others as well.

02:32 Tony: Well, it's massive. Yeah, because they were sort of bumping around that sort of average and sort of getting towards that top level, but we can see there, they've actually dropped away and there’s a little bit of work for them to do. So, we won't focus on that today though, we had a look at them previously. What I'd like to look at though, is this, this interesting one, which is Chase. So we can see there, one of the things that they tend to do, we can see here is they jump up and make some improvements, but those improvements are short- lived. So, it's a bit like whack-a-mole I suppose, that they fix these things and then they sort of drop away and maybe something else turns up as another problem. So we can see here in May, there's been a pickup. So I suppose the question is, what's happened is the first question. May has improved from about 3.2 up to about 3.7, somewhere around there, about a 0.5 improvement. That'd be great to understand what's happened there, but also have a think about what can be maintained and they can just sit around that level of 4 for a longer term.

Let me jump into the next view here. This is just looking at Chase and what this view is, it shows us what's happened with this score across time. Chase were averaging around 3. The most recent spike they had up to 4, and now hitting at 3.8, moving up from 3.3. So, a nice 0.5 improvement.

So what's happened there?

Broadly what we can see down the bottom there are things like Reliability. For example, Unreliable App is 9.8. It was 6.1 points higher.

We can see it on the right here. So it was about 15 to 16 in April and that is now improved down to down to about 10.

Now, of course, these are pain points so the lower the frequency, the better. You want these as low as possible. And we can see things like, App Not Working has actually decreased from about 4.5 down to 3. So, a 30% improvement. It's dropped down to a nice level.

Let's have a look at a bit more detail here, about what's happened. At a high level, we can see that, just looking at Chase again, and again, the lower the frequency, the better. We can see in terms of this, we can see that, with Functionality, that's actually our SURF model here, it's decreased from about 18 down to about 9%. Reliability has improved from 16 down to about 10. That's what we saw in that first view. This is the numbers in a chart form, and Security is also improved, but they are actually getting reasonably good on Authentication Security, and that's down at about 3%, although obviously that's the place where you need to, if you don't win there customers can't get in to use your app anyway.

Let's have a look at something slightly different that we haven't seen before in this view, looking at Features. So which features have they actually made an improvement on? So, what we can see, what we're seeing here are specific features. Now there's an order to what we're showing here as well. This is the order of importance. The things that people talk about most and the things that people comment on most in their app experience. These are the most common things people use and therefore they are the most important things for people. If you don't get these things right, you are causing yourself a problem with your score and with customers of course.

There's 3 actual standouts here that we think they've actually done a bit of work on. There's probably some Security improvements that have been made, but it's not a major shift. It has gone from 2 to 2.2. So here we're looking at, obviously these are the average scores when people talk about these topics. The higher, the better in this case. One thing here that is clear, App Check Deposit feature has had an improvement. I'd say that they’ve done a fair bit of work on that to move that from 2.6 up to 3.4, and in the similar way we can see with the App Payment feature. So, it's General Payments have actually improved as well from 2.6 to 3.2.

The other one that stands out in these top 10 here is, Viewing Transactions.That was an issue for people previously. They've actually made an improvement on that, up to that 3.1 level compared to 2.5. So yeah, looking at this they’ve pushed improvements in the right areas. There's still some improvements elsewhere to make of course, but what's important though is the idea that, one of the things you need to do when you improve your app is not just think, well, how do I improve my score in general, you need to have a focused effort, and that focus comes down to which features or journey should I actually I focus on, and which are the ones that are most important to customers. So, prioritizing what you're doing is really important.

So, those improvements they've made are good cause they're in that top 10 group of things and that's why their score has moved up 0.5 points. What's important to understand though is how do I compare to others and what's my room still to grow in those areas. What we're looking at here is, just comparing across these, the US Nationals here we can see in here on the first one here, which is our Chase number here, which is at 3.4, we saw for App Check Deposit feature.

Now, one of the things we can see is they're still around 3rd to 4th place along with, Wells is probably similar in that sense, but there's two that are above them. In particular, we can see that U.S. Bank is above them at 4.7. So, at 3.4, while good it's still a gap in there of 1.3 points that can actually improve on that particular thing. There's room to grow there. We can also see with the App Payment feature they're sitting on 3.2, whereas U.S. Bank is sitting on a 4.0. So still, you know, growth, 1.8 growth in that area for them to work on. So if they can focus, systematically prioritizing the things that are most important to customers they can grow that number and maintain it rather than having those dips down.

One of the things I'd like to briefly look at is this Cheque Deposit feature, and just have a look at the comments coming through from those from US Bank. So if I select that, I can see on the right the types of comments coming through now these green numbers here, actually the score given, the rating given for U.S. Bank. We can see there that there is a whole swathe of green - it's everywhere. People love this. There's a few big problems. There's a couple coming through with problems, but mostly people giving fives and they love the experience of what's going on.

Let's just do a quick comparison then to what we're seeing with Chase. They've improved, but we can see in here, when this comes up, that there's clearly room to improve. We do see a smattering of 5s coming through, but we're seeing a lot of this red. It's difficult for people to deposit the paycheck, it's difficult to actually take the scan of the cheque, and various things like that. So you know, hard to deposit a cheque. You can see there's room to improve that smattering of red through there, so there's clearly things for them to still work on and keep that movement that they've had over the past month.

Thank you, Glenn.

09:33 Glenn: Thats fantastic, my friend. And it just goes to show, maybe if you dial in and watch these each month, you might be able to figure out what you can actually focus on in your bank without even paying us but if you do want to know more, you can come in and you can check it out on the website. You can send us an email and we can get you some specific information on you, on your bank and what you can do to improve your app.

Thanks again. Another great session Tony, and we will see you next month.