Executive Summary

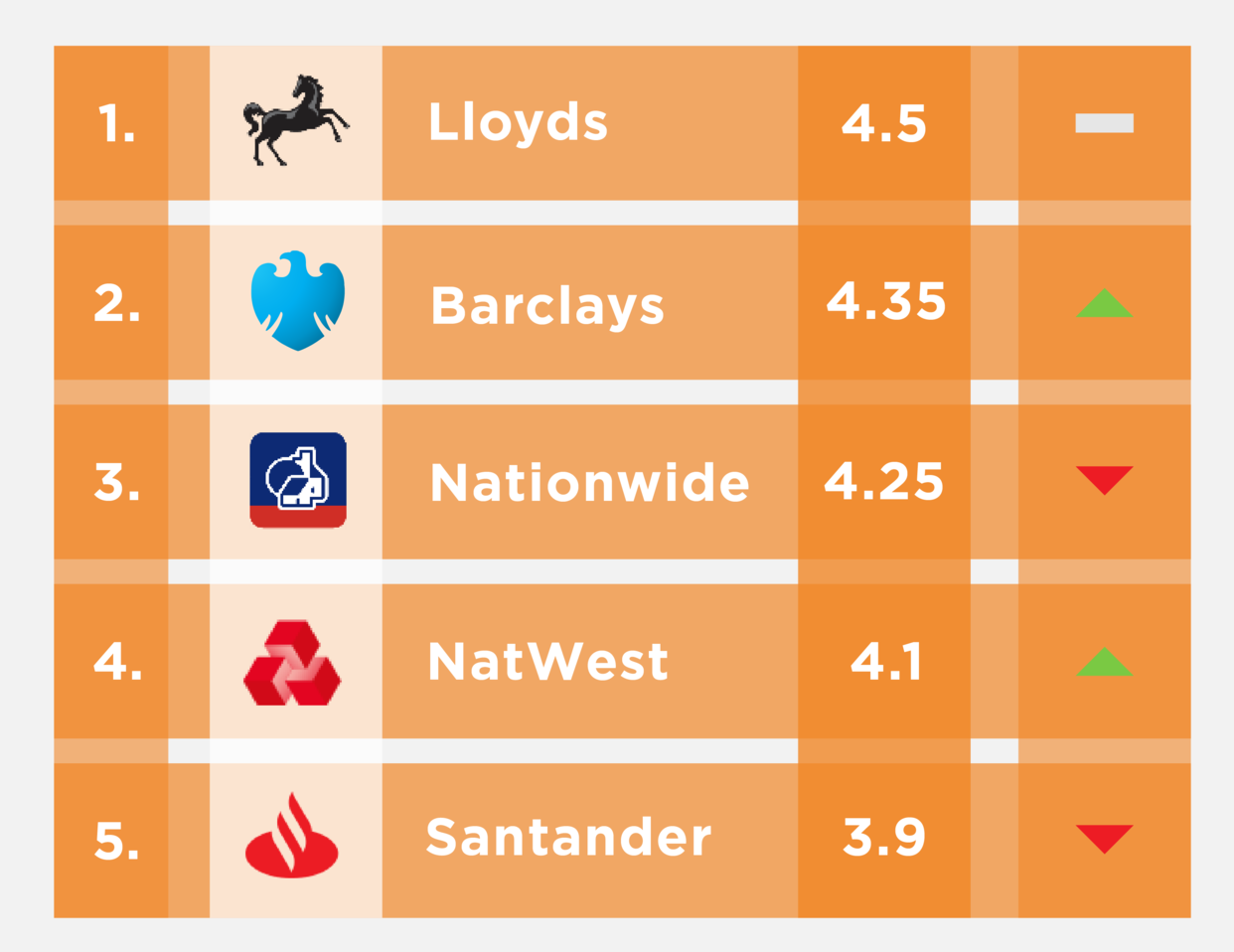

Lloyds and Barclays have maintained positive momentum in May, with Nationwide slipping from 2nd place in Engaged Customer Score (ECS) performance to 3rd place, and NatWest and Santander both continuing their downward slide.

NatWest does however outperform all other Legacy banks in the overall Engaged Customer Score rankings for Core Customer Journeys such as checking balances and depositing cheques in the average ECS.

Santander and NatWest outperformed all other banks with regard to feedback on the contactless payment function.

Lloyds and Barclays dominate the other banks with consistent high performance in all other areas.

Lloyds vs Barclays Performance Improvement Opportunities Insights

One area of opportunity for Barclays to close the gap on Lloyds is the Incremental Banking Features, which are the really important functions of the Current Account, so money in - money out, payments, and everything to do with setting up payees and your standing orders etc.

The Check Deposit feature is where Barclays is ranked practically the lowest of all the Legacy banks, and there is quite a large gap. There's a gap of around 50 basis points on the Engaged Customers Score between Barclays and Lloyds. This show the one feature that Barclays really needs to pay attention to and somehow improve to catch up with Lloyds.

Deeper analysis can also be made on any or all other core features and journeys to identify which areas a bank can prioritize to close the gap or increase dominance over competition.

UK Legacy Bank Engaged Customer Score Performance Rankings As At May 2022

If you would like a free personal deep dive insights session on your banking app performance feel free to book a discovery call.

Full Video Transcript

00:00 Glenn: Hello, and welcome back to another Touchpoint Group insight session in the world of Digital Banking, and more to the point, the UK Legacy banks and their banking apps. It’s the Queen’s Jubilee in the UK, so plenty to celebrate I'm sure. Nick, I'm going to pass it over to you ‘cause I'm sure there's a bit to celebrate for those in the world of banking. What have you got for us this month?

00:26 Nick: We look at the last three months here so we've got a moving average, and this is interesting because if you remember, if you listened to this last month, Nationwide had a rise to the top really based on some excellent work on their mobile app updates. This month you can see that they've slipped back slightly. They're now in 3rd place, and Lloyds has surged ahead again and is now the definite market leader, and then Barclays, which was last month 2nd, sorry, 3rd to both Lloyds and Nationwide, is now very much in 2nd place and they've overtaken Nationwide - an interesting picture. Santander seems to have been going in the opposite direction. So, an interesting kind of divergence now in terms of the distribution of ratings across the top five UK Legacy banks.

01:24 Glenn: Very much so. So let's take a little deeper look shall we?

01:29 Nick: I thought we’d do something different this time and look at if you were Barclays. ‘Cause I mean, Barclays have been kind of snapping at the heels of Lloyds and Nationwide for a while, but I'm just interested in what, if I were them, what would what would I do to try and obtain outright market leadership in engaged app ratings, which is an important KPI in terms of customer satisfaction, brand value, and everything else.

One of the ways to do that is to drill down underneath the topline engaged customer ratings and what we like to do is look at four different levels of customer experience. Now, Level One is Foundational which will be the basic hygiene factors like Reliability and Usability and Security and Operability and so on.

You can see here there isn't really much to choose between the top five. They've all really got this sorted out. So then we move on to level two which is Core Customer Journeys. These are things like Authentication, Mobile app updates, and then basic banking features like the posting of checks and checking your balance.

You can see that interestingly NatWest is the leader in Core Customer Journeys and Lloyds are ranked fairly low and Barclays are doing well there they're second here. Then if we look at the third one which is Incremental Banking Features which are the really important functionality of the current account so money in money out, payments, and everything to do with setting up payees and your standing orders and everything like that.

This is where Lloyds are really ahead. This is the one area I think where Barclays has the most catching up to do because they are about 50 basis points, or half an engaged customer percentage point rating point below Lloyds. So, I thought we'd just drill down a bit further into what comprises the Incremental Banking Features and where could possibly Barclays closed that gap.

These are some of the Incremental Banking Features and you can see that Lloyds is ahead in most of them. Barclays seems to be strong in some and not others. Contactless payments - it seems to be a long way behind. Except that you can see here the sample sizes or the frequency of the reviews is fairly low indicating that might not be a very important feature.

And they're, you know, a little bit behind in spend analysis, but again small sample. So, this is interesting because it does tell you where the gaps are in terms of the gap between Barclays and Lloyds but to do this properly you're missing a piece of information here which is the relative importance of each of these incremental banking features because you really want to fix the important ones, close the gaps in the important ones to really move the needle on the overall Engaged Customers Score.

There are a couple of ways of looking at importance. One is to start to think in terms of the volume of reviews that happen to mention a particular Incremental Banking Feature, how are those distributed? This shows you that. It's effectively saying that of all the reviews that the bank gets, and this is looking at Barclays in particular, most within the Incremental Banking Features, 1.7% are about the check deposit feature and then the next most popular if you like, review topic for Incremental Banking Features is App for your Transactions feature which is 1.5% of the total, not 1.5% of incremental banking features, 1.5%of all the reviews. This is useful. And it would maybe suggest that you need to look at check deposits and that transactions feature, except there's still a missing piece, and that is which of those reviews are positive and which are negative cause you really want to focus your attention on the ones which are negative. If it's positive that's fine.

Here we can actually break them down and this is doing something pretty cool, called Sentiment Analysis and it's actually working out from the language sort of semantics and the kind of tone of the review whether these are negative comments or positive comments.

Here this does throw into relief because it suddenly looks like the app Check Deposit feature for Barclays, it's the one that's attracting the most negative comments and potentially the feature which is dragging down its score relative to Lloyds and the rest of the market the most. Interesting view.

So, is this enough to make a decision that Barclays should focus on app Check Deposits? Nearly, but I think there's one more missing piece of information, and that is what is the gap to the market leader, or to Lloyds for each of these and is Check Deposit feature a big enough gap to make it worth really focusing on? We can look at that as well.

I'm going to start by just looking at the top one which is an Account Statement feature. Barclays is ranked 6 out of 11, but interestingly it's actually the same as Lloyds here. So what this is effectively saying is that if you move the needle on an Account Statement feature you would get above Lloyds but you wouldn't necessarily close a large gap on Lloyds cause it's already level pegging.

Let's just go back to the Check Deposit feature and there we can see Barclays is ranked practically the lowest of all the Legacy banks and there is quite a large gap. There's a gap of around 50 basis points on engaged customers score between Barclays and Lloyds. So, this does really show I think that the one feature that Barclays really needs to pay attention to and somehow improve in order to catch up with Lloyds is the Check Deposit feature.

The question is then what would they need to do? We can look at some of the verbatim comments to give us a clue. First of all we'll look at the verbatims about the Barclays app Check Deposits feature and that is showing us that there are issues it seems around photographing the check, the scanner process, and so on, and so forth. That seems to indicate something around the way that the app is set up to take an image of the check in order to be able to pay it in. Then if you compare that with the Lloyds experience, sorry, this is the NatWest experience because they're the market leaders in this. They seem to have got this sorted.

If there was a role model for Barclays, if they can learn from somebody else's implementation of this feature, probably the one to look at would be NatWest, and we happen to know that NatWest came relatively late to the party with this feature so they were probably able to learn from others as well.

08:30 Glenn:That is an absolutely fascinating deep dive and we're nearly at our time limit so we're going to call it quits there.

If you want some of this information you can check it out on our website, and we do actually also have a slide deck with each of those images on there.

If you want to look at it a little bit closer, sing out, flick us a message.

And we will see you next month with some more incredible insights from this man. Thanks folks.