Executive Summary

The Wells Fargo resurgence continues following the dramatic drop off in Engaged Customer Score (ECS) in February when the bank released a major UI update.

Currently sitting above 3.5 ECS which is a good jump up from where it bottomed out in Feb 2022 at 2.5 but there is still a long way to go to get back to the previous rolling averages over 4.0.

CitiBank and US Bank have consistently been performing well with US Bank surging ahead in April with an Engaged Customer Score of 4.8

Deeper Dive Into the Banking App Performance of Capital One

Capital One has been performing well but very slowly dropping away. It has been sitting at or just below an Engaged Customer Score of 4.25

When we break it down and look at operating system iOS has had a slight drop heading into April but Android users have been experiencing and commenting on more pain points.

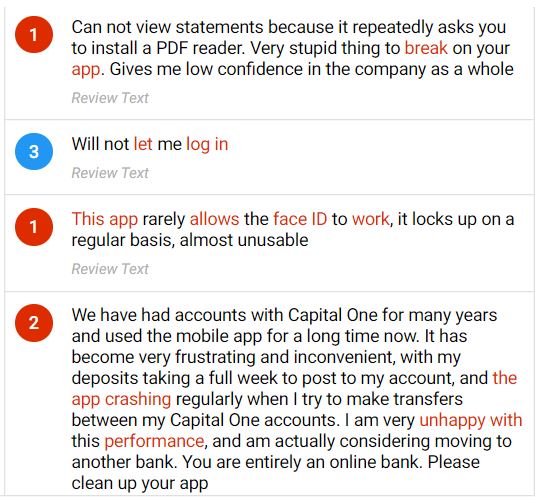

Looking at the Capital One SURF analysis (Security & Authentication, User Interface, Reliability and App Features) we can see that Security & Reliability issues have been one of the major contributors to the gradual decline.

Technical issues include poor authentication - signing in and logging in and these appear to be related to the update version 5.95.13 and people are complaining about the frequency of updates and the poor experience they are having with them.

Feel free to subscribe below to be notified when we release new banking app market insights sessions each month

Full Video Transcript:

00:00 Glenn: Hi everybody. Glenn Marvin here welcome to another Performance Insights Session for the US National Bank segment for April of 2022. This month we're going to have a little bit of a look at the continued resurgence of Wells Fargo since they had their update. In particular we're going to look at Capital One and the journey that they've been on over the last 12 months. I have with me Head of Intelligence, Tony Patrick. Tony, I'll pass it over to you because there's a lot to go through, and as usual, not much time.

00:54 Tony: Great. Thanks, Glenn. I'll jump straight into it then. So, today we're covering off, as Glenn mentioned, the US National Banks, and you'll see there, it covers Wells Fargo, Citibank, Bank of America, Chase, and Capital One. We'll have a look at those today, and how they're moving into April, and what the trends have been. So, let's have a look at what we've found.

There's a lot of chart going on here, but let’s just have a look at what we got. So, what this score actually is, which is important, is one of those questions I've had across this webinars series, is what is this number? It'snot quite the same as what I'm seeing on my app store rating for example.

What we're looking at here is actually what we call an engaged customer score. So it's those people who have given a score and a rating on any of your iOS or Android stores. So what's important about that is, these people are engaged. They've got something to say, they've got something important to tell the business, and it makes this a very much more sensitive measure than what you see elsewhere.

Things on the app store, you might see your score is sitting at 4.1 continuously on the app store, but that could be an average across the past two years. So, it doesn't tell you much about the current situation. It just tells you on average over the past two years your score is whatever it might be. So, here it's a very sensitive measure which is why we can see things in here.

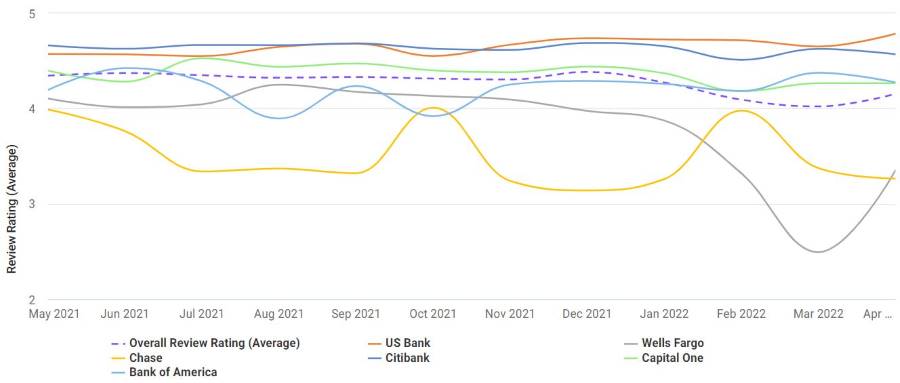

There's a clear one here. If I just put my mouse up at Wells Fargo, we've talked about this previously that there was a drop into March and we can see that Wells Fargo is doing a very good job of potentially educating customers because they've had a bit of a UI change and a major app update, and it takes a while for that to move forward, and so then customers can take full advantage of that to actually then move Wells Fargo’s score back beyond what it was previously.

And we can see where it was previously. It was sitting sort of around between 4 and 4.25 continuously, but it did drop away. Now, if I look briefly, what I can do here is, if I look at Wells Fargo across weeks, we can sort of see where its journey has been taking it across this time.

So if I jump into here and I'll just clear away the others because there's a lot here week-by-week, clear away Citi, Capital One, Bank of America, and just look at Wells Fargo on its own. What we can see there, it has sort of, well, not quite plateaued, but it has moved and jumped around a bit, but it has jumped up substantially since that low point in March.

We can see there, it's heading above 3.5 at the end of April. And so it has, it's definitely improving, but it’s got a little bit of room to move. So, expect in the next sort of maybe six to eight weeks for it to get back to that normal level and potentially increase because of those new improvements. What I'll do here though, there's something interesting I've seen in this data this month that's intriguing.

What I'll do also, it's this one here, which is Capital One. Capital One has been bumping around near 4.5 and also up against the top two there, which is our CitiBank and US Bank, but what's happened over the past three months? You can see it's actually dropped away. It's continuously sitting at, or just below 4.25.

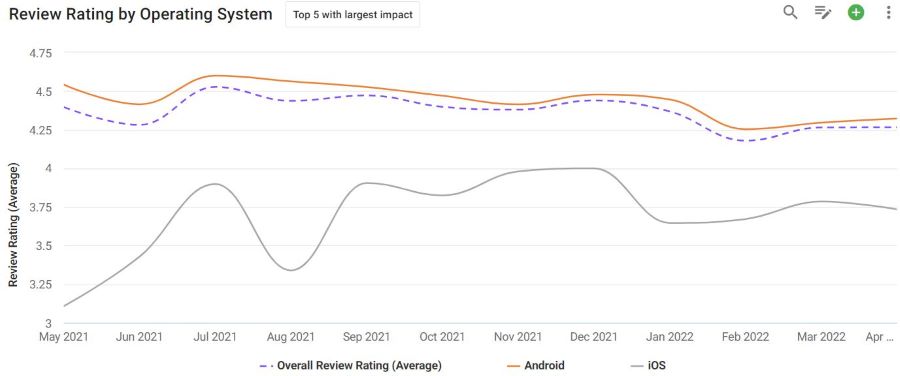

Although not a major movement, that's something you need to be aware of because we're seeing banks previously that moved down slightly, but that continues across time, and if you don't fix those things this can erode. So, let's step into Capital One and see what's happened over that time. This next view here is having a look at just Capital One and having a look at iOS versus Android.

Now, iOS has a lot fewer base, a lot fewer people giving that feedback, but you can see there, it has had a slight drop into January, into April, but pretty much the big move is coming from this drop down here from Android. So something's happened there and we can see a bit of moving across time down as well. So, let's move forward and see what else might be going on there.

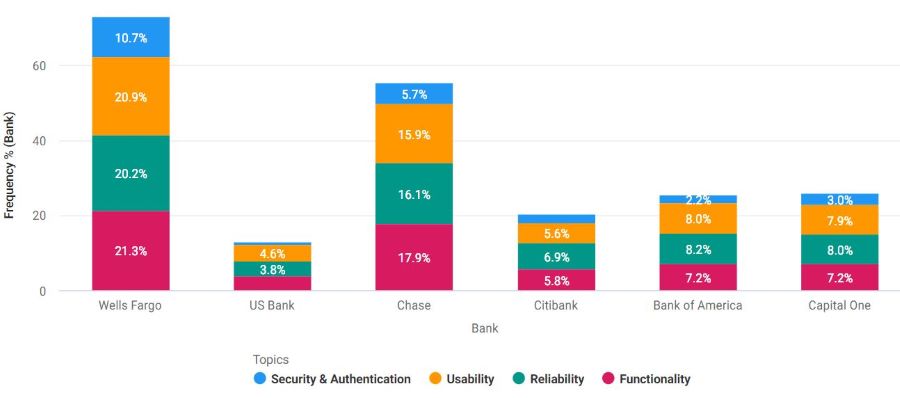

For those familiar with this, you'll understand exactly what's going on, but for others, I'll just introduce this again here, I might actually get the order in the way we described this. This is what we call a SURF analysis. We look at four key areas where you need to perform to be the best in the market. We look at Security and Authentication, Usability, Reliability, and Functionality. What we're looking at here are pain points, so lower is better.

One of the things we've found is if you are getting below 20% you can start to lead the market. We can see why US Bank is so good, doing so well. They have so few pain points across these four key areas to only say 4.1% talking about functionality issues, and at the other end here, when they got about less than 1% talking about Security and Authentication or Login issues, whereas others are getting well beyond that. Even for Wells Fargo up to about 11% on this side here, but let's look at the area of focus here, which is Capital One.

We can see there, they're doing reasonably well, but there's a few areas that they need to improve on. Let's see how they've gone across time though, because that's an important piece. We can see here, this, and this represents what we saw in the score where it’s declined over February into April. It seems to have peaked in March.

So, potentially they’re on the way to improving that, but we can see there how it's impacted the score and its reflected here as well, and on each of these, we can have a look at, for example, where has this come from? We can come down to things like we can see there's been security issues in there as well.

We can see there's a few reliability problems that have also popped up at the same time. So what we can do though, is have a look at a bit of detail. So let's look at that now.

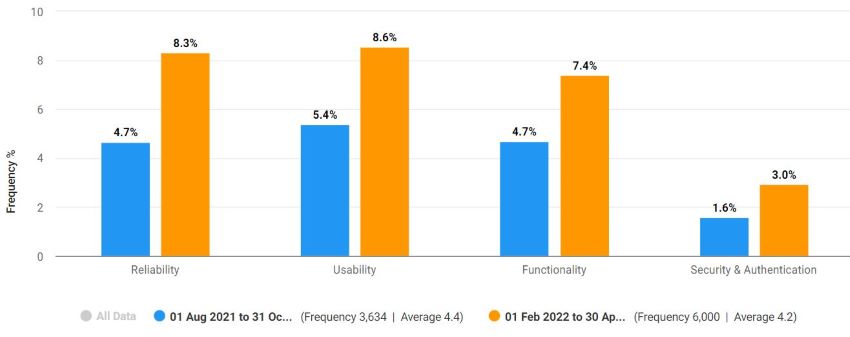

So what I'm doing now is I am, I'm looking at, I've gone down a bit of detail here. So, what I've done is seeing which specific things have actually gone wrong. One of the things we can see here is that there's technical issues in general, but also I can see things about a bad mobile app update and poor authentication. On the right here, I've just had a look at poor authentication and just selected that particular area there. There's issues with signing in and logging in.

There's the authentication thing. People can't log in at all and, or even this person who gave a four out of five, they've been locked out and there's too many bad attempts to get in. We can see here also, if you can see down here, this has actually come from an update, which is 5.9 5.13, It's with an update that's happened probably around March and April and because what I’m looking at here is looking at the end of last year as compared to these last three months to see what's actually changed.

So that's interesting. There's clearly some issues with logging in and biometrics, but also, this area here, which is probably more than tripled, which is about a bad mobile app update and what we can see there when it comes across on the right is the detail of what's happening here.

So, people are saying, “the constant upgrades are annoying”, “I hate the new update, it's hard to use”. Again, looking at this update here, of 5.9, 5.13, so although these people are saying I don't like updates, potentially here, I think they need to do an update to fix what's happening here with those login issues which have appeared recently.

So, that's a pretty good summary of what's going on with Capital One. It's not a major thing. It looks like they have it under control because it's improved slightly into April, but they need to watch out and make sure the new updates actually make a difference and improve things.

08:18 Glenn: Yeah. Thanks for that so much, Tony. I think another great reminder in and around how, it's the granularity that can help you determine what to focus on when that's going to give the greatest impact in regards to improvement. The score is one thing, and it's great for the ego, and it's great to get out there on that, but the reality is when you're getting those improvements in scores you're getting improvement in customer experience, and when you're getting that improvement in customer experience it flows onto that whole bigger picture of retention and revenue.

So again, thank you my friend, looking forward to next month’s insights.

We'll be reminding you, that if you want to get more of these and you want to make sure that you get in there first before everybody else, you can go through to our website for the full version of these and subscribe so that you get notified every time we launch any of these market insights.

Thanks folks.